Table of Contents

Financial discussions surrounding publicly recognized individuals frequently reference a specific measure of economic standing. Celebrity net worth represents an attempt to quantify the total financial position of individuals operating in recognition-oriented industries, expressed as a single summary figure.

Understanding celebrity net worth requires examining what this measure actually represents, how it differs from other financial concepts, and why publicly available figures may not accurately reflect actual financial positions. The concept involves complexity that simple numerical statements often obscure.

What Celebrity Net Worth Means

Celebrity net worth refers to an estimate of the total financial value attributed to a publicly recognized individual at a given point in time. This measure attempts to capture overall economic position by calculating the difference between what someone owns and what they owe.

Net worth functions as a snapshot measure rather than a flow measure. It represents accumulated financial position at a specific moment rather than ongoing financial activity. The figure changes as assets and liabilities change over time.

The celebrity dimension of this concept reflects public interest in the financial positions of recognized individuals. While net worth applies to anyone with assets and liabilities, the term celebrity net worth specifically addresses estimates concerning publicly known figures.

Net worth represents a balance sheet concept borrowed from accounting and financial analysis. It applies the same fundamental calculation used to assess organizational or individual financial position to individuals whose public status generates interest in their economic circumstances.

The measure provides a single summary figure intended to represent complex financial circumstances. This simplification enables comparison and communication but necessarily loses detail present in underlying financial positions.

Net worth figures appearing in public discussion typically represent estimates rather than verified statements. Access to complete financial information about individuals is generally limited, making precise calculation impossible for external observers.

Net Worth Versus Income: Understanding the Difference

Net worth and income represent fundamentally different financial concepts that public discussion sometimes conflates. Understanding their distinction clarifies what net worth measures and what it does not.

Income as Flow

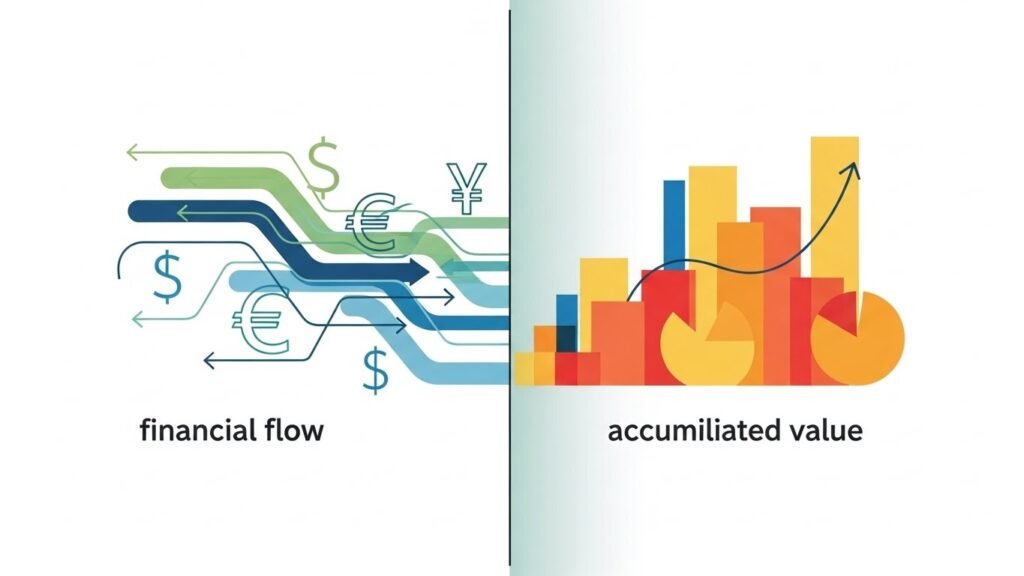

Income represents financial inflows over defined periods. Earnings, revenues, and receipts constitute income that arrives during specific timeframes such as years or months.

Income measures ongoing financial activity rather than accumulated position. High income indicates substantial financial inflows during measured periods but does not directly indicate overall financial position.

Income occurs continuously and varies across different periods. What someone earns in one period may differ substantially from earnings in other periods.

Net Worth as Stock

Net worth represents accumulated financial position at specific moments. It measures what has been accumulated minus what is owed, regardless of current financial inflows.

Net worth changes as assets appreciate or depreciate, as liabilities increase or decrease, and as income is saved or spent. The relationship between income and net worth depends on how income is used rather than income level alone.

High income does not automatically produce high net worth. Income that is fully spent does not accumulate into net worth regardless of its magnitude. Conversely, moderate income that is saved and invested can produce substantial net worth over time.

Relationship Between Measures

Income and net worth relate to each other but measure different aspects of financial circumstances. Income provides resources that may increase net worth, but only the portion that is saved and invested contributes to net worth accumulation.

Public discussion sometimes treats income and net worth as interchangeable or directly proportional. This treatment misrepresents the distinct nature of each measure and the complex relationship between them.

Understanding celebrity net worth requires recognizing that current income levels do not determine current net worth. Financial history, saving patterns, investment outcomes, and liability management all affect net worth independent of current earnings.

Assets Commonly Included in Net Worth

Net worth calculations include assets representing what is owned. Various asset categories contribute to total asset value in net worth calculations.

Financial Assets

Financial assets include cash, bank accounts, investment accounts, and securities holdings. These liquid or near-liquid assets represent readily quantifiable components of net worth.

Retirement accounts, brokerage holdings, and cash equivalents fall within financial asset categories. Their values derive from market prices or account balances that can be determined with relative precision.

Financial asset valuation typically presents fewer estimation challenges than other asset categories. Market prices and account statements provide documentation of values at specific points in time.

Real Property

Real estate holdings constitute significant asset categories for many individuals. Properties owned for personal use, investment, or other purposes contribute to total asset value.

Real property valuation requires estimation based on market conditions. Unlike financial assets with quoted prices, real estate values must be assessed based on comparable sales, appraisals, or other valuation methods.

Property values fluctuate with real estate markets and property-specific factors. Net worth calculations involving significant real estate holdings depend on property valuations that may be uncertain or contested.

Business Interests

Ownership stakes in businesses represent potentially significant net worth components. Equity positions in companies, partnerships, or other business entities contribute to asset totals.

Business interest valuation presents substantial complexity. Unlike publicly traded securities with market prices, private business interests require valuation methods that involve judgment and uncertainty.

The value of business interests depends on business performance, industry conditions, and valuation methodology applied. Different approaches to business valuation can produce significantly different asset values.

Other Asset Categories

Additional asset categories may include intellectual property, royalty streams, collectibles, vehicles, and other property. These varied assets present different valuation challenges and liquidity characteristics.

Intangible assets such as ongoing royalty rights or intellectual property interests may contribute significant value but present particular valuation difficulties. Future income streams require present value calculations involving assumptions about future performance.

Asset comprehensiveness affects net worth accuracy. Calculations that omit significant asset categories understate actual net worth while inclusion of appropriate asset values supports more complete measurement.

Liabilities and Financial Obligations

Net worth calculations subtract liabilities from assets to determine net position. Various liability categories reduce net worth below gross asset values.

Debt Obligations

Outstanding debts reduce net worth by representing claims against assets. Mortgages, loans, and credit obligations all constitute liabilities that offset asset values.

Debt secured by specific assets affects net position in those assets. A property worth a certain amount with a mortgage against it contributes only the equity portion to net worth.

Unsecured debts also reduce net worth by representing general obligations. Total debt levels significantly affect net worth calculations regardless of debt type.

Contractual Obligations

Ongoing contractual obligations may represent liability-like claims against future resources. Long-term commitments that require future payment or performance create obligations that may affect net position.

The treatment of contractual obligations in net worth calculations varies. Some obligations may be included as liabilities while others may be excluded depending on accounting treatment and calculation methodology.

Tax Liabilities

Tax obligations represent claims on financial resources that reduce net worth. Accrued but unpaid tax liabilities constitute debts that offset asset values.

Future tax liabilities on unrealized gains present complex treatment questions. Assets with embedded tax liabilities may have different net worth contribution than their gross values suggest.

Tax liability consideration affects how asset values translate to actual available wealth. Net worth figures may not account for tax consequences of converting assets to cash.

How Net Worth Estimates Are Calculated

Public net worth figures result from estimation processes that attempt to approximate actual financial positions. Understanding these processes reveals the nature and limitations of published estimates.

Information Sources

Net worth estimates draw on various information sources available to external observers. Public filings, disclosed transactions, visible assets, and known professional activities provide data inputs.

Some information sources carry legal disclosure requirements. Business ownership, real estate transactions, and certain financial activities may require public disclosure that provides estimation data.

Other information sources involve observation and inference. Visible property, known professional engagements, and reported transactions may inform estimates without providing complete financial pictures.

Estimation Methodologies

Different approaches to net worth estimation produce different results. Methodological choices about what to include, how to value assets, and how to handle uncertainty affect estimates.

Some methodologies emphasize publicly verifiable information, excluding values that cannot be documented. Others incorporate broader estimates including inferred or assumed asset values.

Valuation approaches for difficult-to-value assets particularly affect estimates. Business interests, intellectual property, and other complex assets may receive widely varying treatment across different estimation approaches.

Temporal Considerations

Net worth represents position at specific points in time. Estimates typically attempt to represent current or recent position but may rely on information from different periods.

Financial positions change continuously as transactions occur and values fluctuate. Estimates based on information from different dates may not accurately represent any single point in time.

Publication timing affects estimate currency. Published figures may reflect information available when estimates were prepared rather than current positions.

Why Public Net Worth Figures Vary

Published net worth figures for the same individual often differ across sources. Several factors contribute to this variation.

Information Access Differences

Different sources access different information about financial positions. Variation in available data produces variation in resulting estimates.

Sources with greater information access may produce different estimates than those with limited data. Neither may have complete information, but estimates will differ based on what each source knows.

Information access may also affect estimation confidence. Sources with more information may express estimates with greater precision while those with less data may provide wider ranges.

Methodological Variation

Different estimation approaches produce different figures even from similar information. Methodological choices compound with information differences to produce estimate variation.

Asset inclusion decisions, valuation approaches, and liability treatment all vary across estimators. These methodological differences directly affect resulting net worth figures.

No standardized methodology governs public net worth estimation. Absent uniform approaches, variation in methodology produces variation in estimates.

Timing Differences

Estimates prepared at different times reflect financial positions at those different moments. Position changes between estimation dates produce legitimate variation in figures.

Even estimates published simultaneously may reflect information from different periods. The recency of underlying information affects how current each estimate is.

Financial positions can change substantially over short periods. Transactions, market movements, and business developments all affect net worth in ways that produce temporal variation in estimates.

Verification Limitations

External observers cannot verify actual financial positions. Estimates represent informed attempts rather than confirmed measurements.

This verification limitation means errors may persist uncorrected. Inaccurate estimates may circulate without correction because verification is not possible.

Different estimates may all be inaccurate in different ways. Variation among estimates does not indicate that any particular figure is correct.

The Limits of Public Net Worth Information

Public net worth figures face inherent limitations that affect their reliability and meaning. Recognizing these limits supports appropriate interpretation.

Incomplete Information Access

External observers lack access to complete financial information. Private assets, undisclosed liabilities, and confidential transactions remain unknown to those preparing estimates.

This incompleteness affects estimate accuracy in unknowable ways. What is unknown cannot be assessed for significance, making error magnitude impossible to determine.

Complete financial information is generally available only to individuals themselves and their professional advisors. All external estimates operate with incomplete data.

Valuation Uncertainty

Many assets resist precise valuation. Real estate, business interests, intellectual property, and other assets lack definitive values that estimation can simply record.

Valuation uncertainty means that even complete asset inventories would not produce precise net worth figures. The values of assets themselves are uncertain, not merely unknown.

Different but reasonable valuation approaches may produce substantially different asset values. This reasonable variation affects net worth estimates without any approach being clearly incorrect.

Dynamic Positions

Financial positions change continuously while published estimates remain static. Published figures may become outdated quickly as transactions and market movements alter actual positions.

The dynamic nature of net worth contrasts with the static nature of published estimates. A single figure cannot capture a continuously changing position.

Major transactions or market events can produce rapid, significant net worth changes. Published estimates may not reflect recent developments that substantially affect actual position.

Common Misunderstandings About Celebrity Net Worth

Several misunderstandings commonly affect how celebrity net worth figures are interpreted. Clarifying these misconceptions supports more accurate understanding.

Precision Assumption

Assuming that published figures precisely represent actual net worth overestimates estimate accuracy. Figures presented to specific amounts suggest precision that underlying estimation processes cannot support.

Net worth estimates typically represent approximate magnitudes rather than precise values. Order-of-magnitude accuracy may be more realistic expectation than exact figure accuracy.

Precise presentation of imprecise estimates creates misleading impressions. Interpretation should recognize that apparent precision reflects presentation choices rather than measurement accuracy.

Liquidity Assumption

Assuming that net worth represents readily available cash misunderstands asset composition. Net worth includes assets that may not be easily converted to cash.

Illiquid assets contribute to net worth calculations but do not represent immediately accessible funds. Real estate, business interests, and other assets may require extended time to convert to cash, potentially at different values than net worth calculations assume.

Net worth and available cash can differ substantially. High net worth individuals may have limited liquidity while lower net worth individuals may have greater immediate access to their assets.

Stability Assumption

Assuming that net worth represents stable, permanent position misunderstands its temporal nature. Net worth fluctuates with asset values, transactions, and financial events.

Published figures represent estimates at particular moments rather than enduring values. Actual positions continue changing after estimates are prepared.

Financial circumstances can change dramatically in short periods. Today’s net worth may differ substantially from recent past or near future positions.

Income Equivalence

Treating net worth as directly indicating income misunderstands the relationship between these measures. High net worth does not necessarily indicate high current income, nor does high income necessarily indicate high net worth.

Net worth reflects accumulated position while income reflects current flows. Their relationship depends on saving, investment, and spending patterns over time.

Comparing individuals on income versus net worth can produce different orderings. Position on one measure does not determine position on the other.

Why Net Worth Attracts Public Interest

Public interest in celebrity net worth reflects several underlying interests and motivations. Understanding these interests helps explain why net worth figures receive attention.

Status Quantification

Net worth provides numerical expression of financial success. This quantification enables comparison and ranking that qualitative assessments do not support.

Numbers communicate concretely in ways that descriptive characterizations do not. Net worth figures provide specific measures that feel more definite than general statements about financial position.

The reduction of complex financial circumstances to single figures supports simplified understanding. This simplification, despite its limitations, appeals to interest in accessible comprehension.

Success Measurement

Financial position serves as one measure of professional success. Net worth provides an outcome measure that may be seen as indicating career achievement.

Interest in professional success in recognition-oriented industries may extend to interest in financial outcomes of that success. Net worth figures provide one indicator of how professional achievement has translated to financial results.

Comparative interest may drive net worth attention. How individuals compare to others on financial measures satisfies comparative interests that drive much public attention to recognizable figures.

Economic Curiosity

General curiosity about economic circumstances motivates interest in financial information. Net worth figures provide information about economic aspects of individuals’ circumstances.

This curiosity reflects broader interest in understanding how different professional circumstances translate to financial outcomes. Net worth provides data addressing these interests.

The scale of figures in recognition-oriented industries may attract particular interest. Financial outcomes that differ substantially from typical experience draw curiosity attention.

Conclusion

Celebrity net worth represents an estimate of total financial position calculated by subtracting liabilities from assets. This measure provides a snapshot of accumulated financial standing at specific points in time.

Net worth differs fundamentally from income. Income measures financial inflows during periods while net worth measures accumulated position at moments. The relationship between these measures depends on saving and investment patterns rather than direct proportionality.

Assets included in net worth calculations encompass financial assets, real property, business interests, and other property. Liabilities including debts, contractual obligations, and tax liabilities reduce net worth below gross asset values.

Net worth estimates result from processes using available information and chosen methodologies. Information limitations, valuation uncertainty, and methodological variation all affect estimate accuracy.

Published net worth figures vary across sources due to information access differences, methodological variation, timing differences, and verification limitations. This variation reflects estimation challenges rather than necessarily indicating any source’s superiority.

Inherent limitations affecting public net worth information include incomplete information access, valuation uncertainty, and dynamic positions. These limitations constrain how accurately external estimates can represent actual financial positions.

Common misunderstandings about celebrity net worth include assumptions of precision, liquidity, stability, and income equivalence. Recognizing these misconceptions supports more appropriate interpretation of published figures.

Public interest in celebrity net worth reflects interests in status quantification, success measurement, and economic curiosity. These interests explain attention to net worth figures despite their limitations.

Celebrity net worth, properly understood, represents imprecise estimates of complex financial positions rather than definitive measurements of precisely determined values. This understanding supports appropriate interpretation of figures that circulate in public discussion.